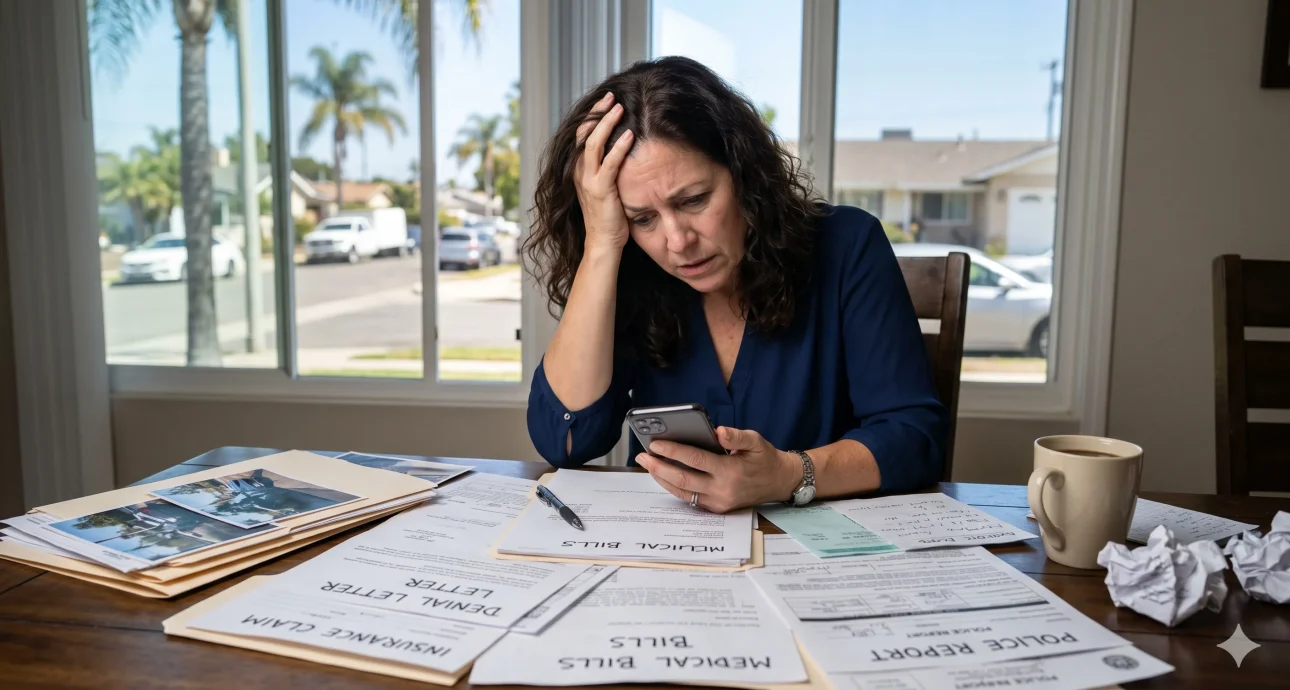

A car accident can turn ordinary life into paperwork, pain, missed work, vehicle repairs, medical appointments, and constant calls from insurance adjusters. The process becomes even more frustrating when the insurance company that is supposed to handle the claim fairly starts delaying, denying, underpaying, or ignoring the facts.

That is where bad faith insurance becomes important. Bad faith can happen when an insurance company fails to treat a claim honestly, fairly, and reasonably. For accident victims in San Diego, this can mean waiting too long for answers, receiving a lowball offer that does not reflect the actual harm, being blamed unfairly for the crash, or getting denied without a proper explanation.

At AK Injury Law Firm, a female owned personal injury law firm in San Diego, the approach is built around strategy, preparation, and strong advocacy. Founder and main attorney Dr. Azadeh Keshavarz brings a unique background to personal injury law. Before becoming an attorney, she was a doctor of chiropractic and saw firsthand how insurance companies often treated accident patients. That experience shaped the way she fights for injured clients today. Her firm’s slogan, Outthink, Outfight, Outwin, reflects a smarter way to take on insurance companies.

What Does Bad Faith Insurance Mean?

Bad faith insurance generally means an insurance company did not handle a claim with the fairness, honesty, and reasonable care required under the circumstances. Insurance companies are businesses, but they still have obligations when reviewing, investigating, and responding to claims.

After a car accident, an insurance company may be involved in several ways. Your own insurance company may handle uninsured motorist coverage, underinsured motorist coverage, medical payments coverage, collision coverage, or other benefits under your policy. The other driver’s insurance company may be responsible for evaluating your injury claim if their insured caused the crash.

Bad faith issues are often most direct when your own insurer wrongfully refuses to provide benefits owed under your policy. However, unfair tactics can appear throughout the claims process, including negotiations with the at-fault driver’s insurer. The key issue is whether the company acted reasonably or used delay, denial, pressure, or misrepresentation to avoid paying what the claim is worth.

Common Examples of Bad Faith Insurance Tactics

Insurance companies do not always announce unfair conduct clearly. Many bad faith tactics are subtle. They can look like “normal processing” at first, but over time the pattern becomes harder to ignore.

Unreasonable Delays

One of the most common signs of bad faith is delay. The insurance company may keep saying it needs more time, more records, more statements, or more review. Some delays are normal, especially in serious injury claims. But when the company has enough information and still refuses to act, delay may become a pressure tactic.

Delays can hurt accident victims because medical bills continue, income may be interrupted, and stress builds. The longer an insurance company waits, the more likely an injured person may feel forced to accept less than the claim is worth.

Lowball Settlement Offers

A low offer is not always bad faith by itself, but it can be a warning sign when the offer ignores medical evidence, wage loss, pain, long-term effects, or clear liability. Some insurers make early settlement offers before the full extent of the injury is known.

This can be especially dangerous after car accidents because symptoms may worsen over time. Neck injuries, back injuries, concussions, nerve pain, and soft tissue injuries may require ongoing care. If an injured person settles too early, they usually cannot reopen the claim later simply because the injury turned out to be more serious.

Denying a Claim Without a Fair Investigation

An insurance company should not deny a claim before reasonably reviewing the evidence. A fair investigation may include police reports, medical records, witness statements, photos, repair estimates, crash details, policy language, and liability facts.

When an insurer denies a claim without gathering important information, ignores evidence that supports the injured person, or relies only on information that benefits the insurance company, the denial may be unfair.

Misrepresenting Policy Language

Policy language can be confusing. Insurance companies may use that complexity to their advantage. A bad faith issue may arise when an insurer misrepresents what the policy covers, leaves out important policy benefits, or tells a claimant that coverage does not apply when the facts or policy suggest otherwise.

This is why it is important not to rely only on what an adjuster says over the phone. The policy, the facts, and the law all matter.

Failing to Communicate

A claim should not disappear into silence. If calls, emails, letters, or document submissions are repeatedly ignored, that may be a red flag. Insurance companies are expected to respond to claim communications within reasonable timeframes.

Lack of communication can create confusion and pressure. Injured people may not know whether their claim is still being reviewed, what documents are missing, or why payment has not been issued.

Why Bad Faith Insurance Happens After Car Accidents

Car accident claims often involve several financial pressures for insurance companies. The insurer may want to reduce payouts, avoid setting a precedent, minimize medical damages, dispute liability, or pressure the injured person before they hire an attorney.

Insurance companies may also use claim software, internal evaluation systems, and adjuster tactics designed to reduce the value of injury claims. A person without legal representation may not know how to challenge these systems or identify when the insurer is ignoring important evidence.

That is why strategy matters. Fighting an insurance company is not just about being aggressive. It is about knowing what evidence matters, how insurers evaluate claims, where their arguments are weak, and how to build pressure at the right time.

Signs That an Insurance Company May Be Acting in Bad Faith

Not every difficult claim is bad faith. Some claims are complicated because liability is disputed, medical treatment is ongoing, or multiple insurance policies may apply. Still, there are warning signs that should be taken seriously.

- The insurer keeps delaying without a clear reason.

- The adjuster refuses to explain the denial in writing.

- The company ignores medical records or key evidence.

- The settlement offer is far below the documented damages.

- The insurer blames you without strong evidence.

- The adjuster pressures you to settle quickly.

- The company asks for unnecessary or repetitive documents.

- The insurer misstates what your policy covers.

- The company refuses to acknowledge communications.

- The insurer changes its reason for denial repeatedly.

If several of these signs appear together, it may be time to speak with a personal injury attorney who understands insurance strategy and bad faith tactics.

What Should You Do If You Suspect Bad Faith?

The way you respond can affect the strength of your claim. Insurance companies document everything. You should too.

Keep Every Communication

Save emails, letters, claim numbers, voicemail messages, text messages, and adjuster notes. If you speak with an adjuster by phone, write down the date, time, name of the adjuster, and what was discussed.

Ask for Explanations in Writing

If your claim is delayed, denied, or underpaid, ask the insurer to explain the decision in writing. Written explanations make it harder for the company to change its story later.

Do Not Accept a Quick Settlement Without Understanding Your Injuries

Once you sign a settlement release, your claim is typically over. Before accepting payment, make sure you understand your medical condition, future treatment needs, lost income, pain, and long-term impact.

Get Medical Care and Follow Treatment Recommendations

Insurance companies often attack gaps in treatment. They may argue that you were not seriously injured or that something else caused your symptoms. Consistent medical care helps protect your health and your claim.

Speak With a Personal Injury Lawyer

An experienced attorney can review the insurance company’s conduct, gather evidence, calculate damages, communicate with adjusters, and determine whether the insurer is acting unfairly.

How a Lawyer Can Fight Bad Faith Insurance Tactics

A strong personal injury lawyer does not simply argue with the insurance company. The lawyer builds a case that makes the insurer’s position harder to defend.

At AK Injury Law Firm, the strategy is not just to fight harder. It is to fight smarter. Dr. Azadeh Keshavarz understands injury cases from both a medical and legal perspective because of her background as a doctor of chiropractic. That experience helps her understand how accident injuries affect the body, how treatment records should be evaluated, and how insurance companies may try to minimize legitimate pain.

A lawyer may help by:

- Reviewing the policy to identify available coverage and insurer obligations.

- Investigating the accident through police reports, photos, witness statements, and expert analysis when needed.

- Documenting injuries with medical records, provider opinions, imaging, treatment plans, and long-term care needs.

- Calculating damages including medical bills, future care, lost wages, reduced earning ability, pain, suffering, and life disruption.

- Challenging unfair denials with evidence and legal arguments.

- Responding to lowball offers with a clear demand supported by documentation.

- Preparing for litigation when the insurance company refuses to act reasonably.

Why Strategy Matters More Than Noise

Some people assume the best way to handle an insurance company is to be loud, angry, or confrontational. That may feel satisfying, but it is not always effective. Insurance companies are used to complaints. What they respond to is leverage.

Leverage comes from preparation. It comes from knowing the policy, proving liability, documenting damages, showing the long-term impact of injuries, and making the insurer understand that the case is ready for the next step.

That is the heart of Outthink, Outfight, Outwin. First, you outthink the insurance company by understanding its tactics and weaknesses. Then, you outfight by building a stronger case than the insurer expected. Finally, you outwin by pursuing the result the client deserves with focus and discipline.

Bad Faith and Car Accident Victims in San Diego

San Diego drivers face accidents on busy roads, freeways, intersections, and coastal routes every day. Crashes on I-5, I-8, I-15, SR-163, SR-52, and city streets can lead to serious injuries and complex insurance claims.

After an accident, insurance companies may try to reduce the value of a claim by arguing that the injuries were pre-existing, treatment was excessive, property damage was minor, or the injured person recovered quickly. These arguments may not reflect the real impact of the crash.

For many accident victims, the most frustrating part is feeling unheard. They know how much pain they are in. They know how the crash changed their work, sleep, family life, and daily routine. But the insurance company may treat the claim like a number on a screen.

A strategic lawyer can change that dynamic. Instead of allowing the insurer to control the story, the attorney can present a clear, evidence-based narrative showing what happened, why the insurer is responsible, and how the injury affected the client’s life.

What Damages May Be Involved in a Bad Faith or Injury Claim?

The damages available depend on the type of claim, policy, facts, and legal issues involved. In a car accident injury claim, damages may include:

- Emergency medical care

- Chiropractic care, physical therapy, or specialist treatment

- Imaging, testing, injections, surgery, or future medical care

- Lost wages

- Loss of earning ability

- Pain and suffering

- Emotional distress

- Vehicle damage and related losses

- Out-of-pocket expenses

In certain insurance bad faith matters, additional damages may be possible depending on the insurer’s conduct and the legal relationship between the claimant and the insurance company. Because these cases are fact-specific, an attorney should review the situation carefully before making any conclusion about potential recovery.

Why Dr. Azadeh Keshavarz’s Background Matters

Dr. Azadeh Keshavarz did not enter personal injury law from a distance. Before founding AK Injury Law Firm, she worked as a doctor of chiropractic and saw accident patients dealing with pain, financial stress, and insurance pushback. She witnessed how injured people could be treated as problems instead of human beings.

That perspective matters because injury cases are not only legal cases. They are medical stories, financial stories, and personal stories. A lawyer who understands how injuries affect the body can better understand treatment records, symptom patterns, recovery challenges, and the tactics insurers use to minimize claims.

As the founder of a female owned personal injury law firm in San Diego, Dr. Keshavarz brings both compassion and strength to the claims process. Her firm fights insurance companies with strategy, not guesswork.

How to Protect Yourself During the Insurance Process

The steps you take after a crash can make a major difference. Even if the insurance company has not acted in bad faith yet, protecting yourself early can help prevent mistakes.

- Report the accident and keep copies of all claim information.

- Take photos of vehicles, injuries, road conditions, and the accident scene when possible.

- Get medical care quickly and follow the treatment plan.

- Avoid recorded statements without understanding how they may be used.

- Do not guess about your injuries, speed, fault, or medical future.

- Do not post about the accident on social media.

- Do not sign releases before legal review.

- Contact an attorney if the insurer delays, denies, underpays, or pressures you.

When Should You Call a Lawyer?

You should consider calling a lawyer as soon as the insurance process feels unfair, confusing, or aggressive. You do not need to wait until the claim is denied. In many cases, early legal involvement can prevent the insurer from gaining control of the claim.

You should contact an attorney if the accident caused significant pain, medical treatment, missed work, long-term symptoms, disputed fault, uninsured or underinsured driver issues, or a settlement offer that does not seem fair.

A lawyer can step in, protect your rights, and handle the insurance company while you focus on recovery.

How We Can Help

At AK Injury Law Firm, we help San Diego car accident victims fight back when insurance companies delay, deny, underpay, or refuse to take injuries seriously. Led by Dr. Azadeh Keshavarz, our female owned personal injury law firm brings a unique combination of medical insight, legal strategy, and determined advocacy to every case. We do not fight blindly. We build smart cases, expose weak insurance tactics, and pursue the compensation our clients deserve. If you believe an insurance company is treating your claim unfairly, AK Injury Law Firm is ready to help you Outthink, Outfight, Outwin.